General

Publications & Data

Join the conversation

Social Links

Social Links

It was a week filled with geopolitical upheavals. The fallout from President Ramaphosa’s ill-timed signing of the Expropriation Bill (covered in this Weekly) continued to unfold. Just as tensions between the ANC and DA within the GNU appeared to be shifting toward constructive dialogue, US President Donald Trump chimed in on Sunday on social media. Trump announced that the US would cut all aid to SA due to SA’s confiscation of land and the poor treatment of “certain classes of people”. SA President Ramaphosa was quick to respond to Trump. While SA is not reliant on US aid, America’s President's Emergency Plan for AIDS Relief (Pepfar) initiative supplies 17% of the funds for SA’s HIV/Aids programme. Relations between the US and SA remained strained with the US Secretary of State Marco Rubio announcing that he would not be attending the G20 summit in SA later this month. Rubio has, among other problems, taken issue with SA “using the G20 to promote solidarity, equality and sustainability”.

Beyond SA, Trump had a busy week. After imposing a 25% tariff on Canadian and Mexican imports last week – set to take effect on the 4th of February – he delayed implementation by 30 days. This followed discussions with Mexican President Claudia Sheinbaum and Canadian Prime Minister Trudeau and them pledging to address US concerns, particularly regarding border security. Trump did implement a 10% tariff on Chinese imports. In response, China imposed tariffs of 10 - 15% on US goods, including liquefied natural gas, coal, and crude oil, and announced export restrictions on key minerals used in high-tech industries. Additionally, Beijing launched an antitrust investigation into Google. Trump is expected to speak with Chinese President Xi Jinping in the coming days.

Adding to global tensions, Trump proposed that the US “take over” the war-torn Gaza Strip after permanently resettling its two million Palestinian inhabitants in neighbouring countries. Speaking alongside Israeli Prime Minister Benjamin Netanyahu, he suggested transforming Gaza into the “Riviera of the Middle East.” However, he did not clarify under what authority the US would occupy the territory. The proposal sparked immediate backlash. UN Secretary-General António Guterres urged Trump to “avoid any form of ethnic cleansing,” while key global powers, including Saudi Arabia, rejected the plan.

Shifting the focus back to domestic soil, President Ramaphosa delivered his State of the Nation Address (SONA) on Thursday. President Ramaphosa’s speech focused on key economic and governance reforms while indirectly reaffirming SA’s sovereignty in response to US President Trump’s comments. A key focus of the speech was the Medium-Term Development Plan, which aims to boost economic growth to over 3% through large-scale infrastructure investment. The government plans to spend R940 billion over the next three years on roads, bridges, dams, and waterways. Water infrastructure is set to receive R23 billion for seven major projects. Other encouraging details from the speech include the mention of the review of a funding model for municipalities to improve service delivery on a local level and the implementation of a digital identity system. The Impumelelo Growth Lab recently published a note on the critical reforms required to enhance municipal performance. There was also much talk of leveraging private capital for railway and logistics. The President also confirmed that the Social Relief of Distress (SRD) grant would be used as the basis for the introduction of a grant to support unemployed people. He reaffirmed his commitment to National Health Insurance (NHI) despite opposition, stating that it would reduce healthcare inequality. It should be noted that in his speech, the President referred to preparatory work for the NHI and not its imminent implementation. Considering this, it is unlikely that Treasury will make room for the NHI in its February budget.

In other domestic news, steel producer ArcelorMittal South Africa (AMSA) has extended the shutdown of its long steel business by a month to allow further discussions with the government on potential solutions to prevent closure and to maintain supply for downstream customers with no immediate alternatives. The delay was made possible by a R380 million loan from the state-owned Industrial Development Corporation (IDC), a shareholder in AMSA, which also extended the repayment deadline of a previous R950 million loan from June 2025 to September 2026.

Much of the market's movement this week stemmed from US President Trump’s tariff announcements. As risk sentiment surged, safe-haven assets like the US dollar and gold rose sharply, with gold bullion closing at a record $2,869 per ounce on Wednesday. Both later retreated as the initial shock subsided but still ended the week stronger.

Stock markets initially tumbled as investors digested the weekend developments but some relief set in when Trump suspended levies on goods from Mexico and Canada for a month. Wall Street was further reassured that the situation had not escalated further, particularly regarding counter-tariffs from Beijing. European stocks reached all-time highs, fuelled by strong earnings, while Britain’s FTSE 100 also hit a record peak after the Bank of England (BoE) cut interest rates by 25bs, though it warned of caution amid inflation concerns and geopolitical risks – see the international section below.

SA assets sold off early in the week as, in addition to the jitters in the system following Trump’s tariff announcement, his pledge to end aid over the Expropriation Act rattled local markets. The rand recovered some losses, ending the week ‘just’ 0.2% weaker against the dollar. Bonds followed a similar pattern, with the 10-year yield rising 11bps for the week after spiking by over 20bps on Monday. Despite early losses, the JSE Alsi closed 1.1% higher for the week. Meanwhile, Brent crude prices declined, driven by an improved supply outlook as OPEC+ maintained its plans to gradually increase production from April and growing concerns over global demand amid trade tensions.

Locally, Stats SA will release more real economic data for December (following yesterday’s electricity production release – see the domestic section for more). The December manufacturing and mining production data will give us our first “complete” set of data for the fourth quarter. Both mining and manufacturing added positively to GDP in the third quarter but posted monthly contractions in November. A decline in the December Absa PMI suggests that manufacturing production could see a further downtick in December.

In the US, key economic indicators will shape interest rate expectations. Inflation data and Fed Chair Jerome Powell’s testimony before Congress will be closely watched, alongside today's January nonfarm payrolls report. While job openings and jobless claims suggest a cooling labour market, the Fed is likely to maintain a cautious stance due to potential inflationary risks from trade policy

Meanwhile, in the UK, January retail sales data and Q4 GDP figures will be released. The BoE’s latest monetary policy report projects a 0.1% contraction in Q4 after stagnation in Q3.

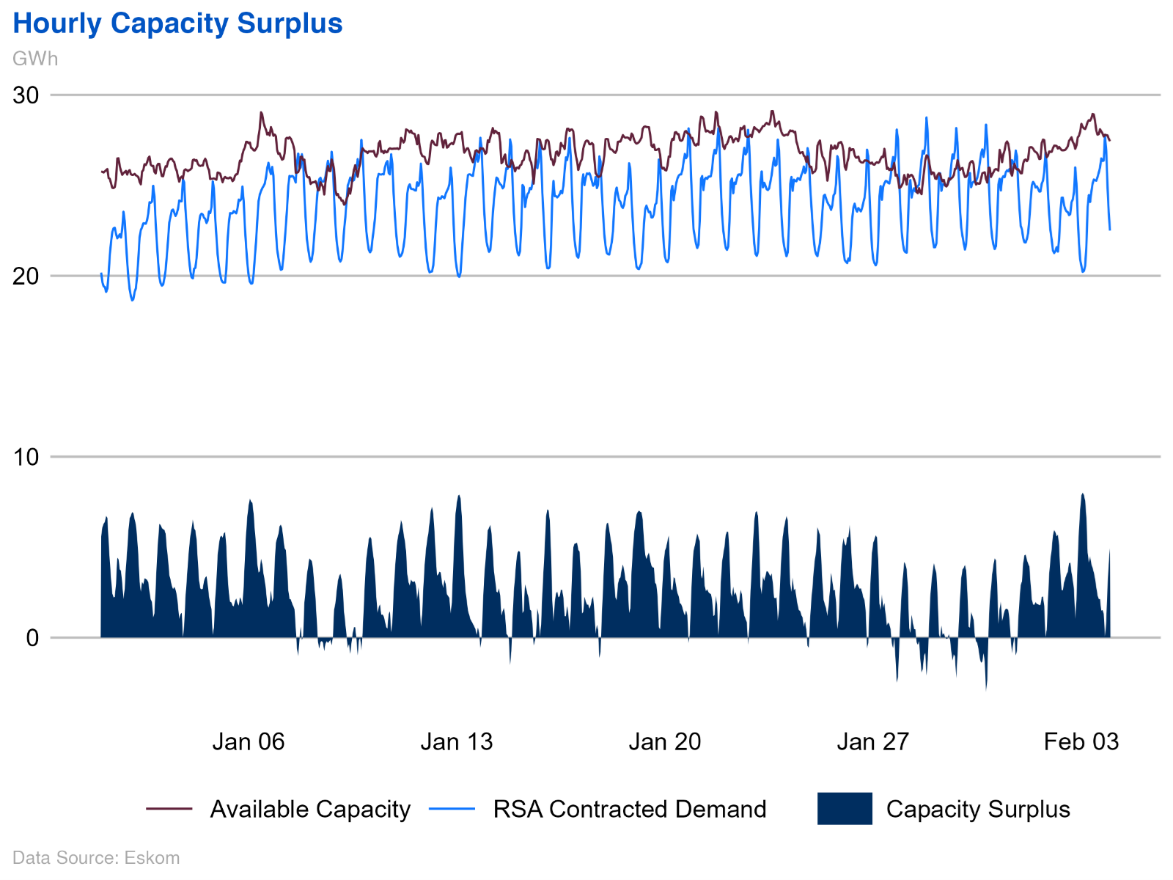

After over 300 days without load-shedding, the reintroduction of power outages at the end of January reminded us that the system is still very constrained. Stage 3 load-shedding was reintroduced on Friday afternoon and lasted until early Sunday morning due to a combination of maintenance delays and technical failures, which Eskom described as a "perfect storm" of incidents.

The hourly demand and supply figures show the deterioration in available capacity from 27 January. Demand, however, remained strong, and on 31 January, capacity went into deficit.

The return of load-shedding has highlighted that electricity supply conditions remain very tight. The lack of a stable, predictable supply of electricity remains a significant brake on economic growth. However, if growth were to accelerate rapidly, the risk of another round of load-shedding would rise.

It also highlights the need to press ahead with the electricity system reform programme. Already, reforms to create independent power producers have added over 6GW of electricity generation capacity. The unbundling of Eskom will lead to a more competitive generation market, bringing new capacity online.

Note that daily Eskom data is available on the BER Data Playground.

After more than a decade of delays, the government appears to be on track to launch a new mining cadastral system to manage mineral rights and exploration licence applications by midyear. The Department of Mineral Resources and Energy (DMRE) unveiled a prototype model at the Investing in African Mining Indaba in Cape Town, which is reportedly being tested in the Northern Cape.

It is hoped that an efficient, transparent system will reduce turnaround times and eliminate the accusations of bias and manipulation that have plagued the current SAMRAD applications process, thus expediting new investment in a sector that has performed well below its potential for many years.

February’s batch of PMI data reflected a tough start to the year. The Absa PMI declined from 46.8 to 45.3 in January, contracting for a third straight month. Owing to declines in the indices tracking employment and inventories, the headline index dropped to its lowest level in five months. Encouragingly, although the activity and demand indices remain in contractionary terrain, both registered modest improvements. In addition to this, despite the index tracking business conditions in six months’ time declining by 2.6 points to 64.9, this still points to manufacturers remaining fairly optimistic about business conditions in the future – click here for the full report.

The S&P Global SA PMI also signalled sluggish activity, down 2.5 points to 47.4 in January. This was driven by weak demand conditions, which led to a sharp decline in output. However, easing supply chain and price pressures contributed to a strengthening of optimism towards future activity.

According to naamsa, new vehicle sales started 2025 on a strong note. Benefitting from some windfalls for the consumer (and a low base in 2024), domestic new vehicle sales increased by 10.4% y-o-y in January, with passenger vehicle sales surging by 18.3% y-o-y. Meanwhile, exports rose by 29.7% y-o-y in January.

Lastly, moving back to 2024 data, Stats SA reported that annual electricity production rose by 3.2% y-o-y in December. However, compared to the previous month production declined by 1.4% m-o-m (seasonally adjusted). Indeed, electricity production contracted in Q4 relative to Q3 and will weigh on quarterly GDP growth.

In alignment with expectations, the BoE cut its policy interest rate by 25 bps on Thursday. Although this move was widely anticipated, the likelihood of further cuts hangs in the balance. There is still a lot of pressure on prices, and the BoE expects inflation to reach 3.7% in the middle of the year, far higher than the previous forecast. The currency is depreciating, there is higher-than-expected wage growth, and higher energy prices will likely push up inflation. This weighs against further cuts. Even so, the BoE members voted surprisingly dovish despite their very hawkish forecast. They argued that inflation would follow a bumpy ride towards its target, but for now, some reprieve on the interest rate front was necessary. Economic growth was very disappointing towards the end of last year, and consumer confidence declined, which is why they may be eager to get the economy back to life again.

Flash estimates from Eurostat indicate that annual consumer inflation in the Eurozone increased again in January, rising to 2.5%, up from 2.4% in December. Energy inflation recorded a significant increase, climbing to 1.8% in January from 0.1% in the previous month as the deflationary impact of the base effects from 2023 and early 2024 began to fade.

Meanwhile, service inflation dipped slightly to 3.9% in January but remained persistent. Rising wages are a key driver of this ongoing service inflation. However, the ECB’s wage tracker suggests that wage growth is expected to slow sharply this year, with an estimated increase of 1.5% in the fourth quarter of 2025, compared to 5.3% in the fourth quarter of 2024. This slowdown is likely to have a dampening effect on inflation.

In contrast, wage growth in Japan is accelerating. In December, it rose by 4.8% y-o-y, up from 3.9% in November, significantly exceeding consensus expectations. This December reading is the highest since January 1997.

The January Caixin Manufacturing PMI dropped to 50.1 from 50.5 in December, still indicating growth due to higher manufacturing output, purchasing activity, and inventory levels. Domestic demand drove new orders, while export orders declined. Despite improved sentiment, tariff concerns kept it below average. The NBS Manufacturing PMI fell below 50, which focuses on larger government-owned firms, unlike Caixin’s focus on relatively smaller manufacturers.

The Caixin Services PMI fell to 51 from 52.2, marking a four-month low but still expanding. As such, the Caixin Composite PMI, combining manufacturing and services, decreased to 51.1 from 51.4, staying above the neutral 50 mark.

In the US, the ISM Manufacturing PMI for January reached 50.9, marking its first expansion since October 2022. Key demand indicators showed improvement, with new orders increasing rapidly and new export orders returning to expansion. Factory output also saw gains compared to December. However, the price index continued to rise, indicating growing price pressures.

In other news, the US trade deficit sharply increased in December, widening by $19.5 billion to $98.4 billion, the largest one-month shift since the 1990s. Imports rose significantly, driven by a 19% increase in industrial supplies, likely due to anticipated trade tariffs, while exports declined. The overall trade deficit for 2024 was 17% larger than in 2023.

Editor: Lisette IJssel de Schepper

Tel: +27 (0)21 808 9755

Email: lisette@sun.ac.za

Click here for previous editions of this publication.

Please refer to the glossary on the BER website for explanations of technical terms.

Friday, 07 Feb 2025