General

Publications & Data

Join the conversation

Social Links

Social Links

Tracey-lee Solomon

Another eventful week started with US President Donald Trump’s accusations of human rights violations against white farmers in SA. This accompanied a freeze of all aid towards SA and a promise to allow Afrikaners to apply for refugee status in the US – later in the week, the US said they could be ‘resettled’ in the US. Details on what exactly this means and how it would work remain sparse. On the data front, Stats SA figures showed a decline in both mining and manufacturing production in December and across the fourth quarter. With fourth-quarter GDP figures set for release in March, it is already clear that both sectors will weigh on overall growth. The below-50 January Absa PMI suggests that the factory sector remained under pressure at the start of 2025.

Adding to the economic concerns, the SONA debate sparked some frustration. After promising noises about more agreement among the GNU parties the week before, Health Minister Aaron Motsoaledi denied reports of a deal between the ANC and DA to preserve private medical aid schemes as part of the NHI rollout. This highlights the ongoing need for greater local policy clarity at a time of increased global uncertainty.

While some confusion remains, the US embassy in SA has provided more clarity on PEPFAR – the US President’s Emergency Plan for AIDS Relief – which faced uncertainty following Trump’s executive order halting aid to SA. Given that PEPFAR funds 17% of SA’s HIV/AIDS programme, its potential suspension has raised serious concerns. This week, the US embassy confirmed that PEPFAR activities will resume under a limited waiver granted by US Secretary of State Mark Rubio in January. Initially, only activities covered under the waiver would restart with each agency following its own legal process for resumption; later, it was said that all activities could resume.

On the global monetary policy front, US Fed Chair Jerome Powell's congressional testimony drew significant attention. Powell reaffirmed that the Fed sees no immediate need to adjust its policy stance, a position supported by robust economic data. The labour market remained strong, with unemployment edging lower and hourly earnings rising. In addition, jobless claims fell in early February. Meanwhile, consumer inflation unexpectedly accelerated in January, further above the Fed’s 2% target. However, Powell cautioned against overreacting to a single month of data, emphasising that restrictive policy needs time to bring inflation down.

On Thursday, the January producer inflation report showed a larger-than-expected increase, though some core PCE components (the Fed’s preferred inflation measure) rose less than CPI suggested, indicating that the upcoming core PCE could undershoot expectations. Powell’s remarks and the latest data suggest that policy changes remain on hold for now, with the Fed prioritising patience as it assesses inflation trends.

Conversely, the Reserve Bank of India (RBI) cut its policy rate by 25 basis points (bps) on Friday. This was after headline CPI fell for the third consecutive month and by much more than expected. With another rate cut anticipated in April, India could find itself in a relatively strong position – provided it stays out of Trump’s crosshairs. On Thursday, the Indian President met with Trump to discuss trade. While the two leaders have had a good relationship in the past, Trump has previously criticized India as a 'very big abuser' of tariff disparities, and the US president has promised to implement “reciprocal tariffs”.

Trump’s second term began with a flurry of activity, wasting no time in reshaping US foreign and economic policy whether necessary or not (e.g. Gulf of America). Following controversial comments on how to achieve lasting peace in Gaza, his attention turned to Ukraine this week. In a significant move, after having spoken to Russian President Vladimir Putin, Trump signalled a willingness to negotiate Ukraine’s future without Ukraine or the EU’s involvement. He later spoke with Ukrainian President Volodymyr Zelensky. While Trump did not give specifics, his Defence Secretary, Pete Hegseth, made the administration’s position clear at NATO headquarters. Hegseth stated that the US would not provide troops or aid to enforce any truce. He also dismissed a return to Ukraine’s pre-2014 borders as unrealistic and ruled out NATO membership for Ukraine. European NATO members have long spoken about a path to join NATO for Ukraine. These developments pose serious challenges for Europe, which now faces the daunting task of filling the military void a US withdrawal would create. Some estimates suggest defence spending would need to rise to 5% of GDP, more than double NATO’s 2% target. Additionally, allowing Russia to retain seized territory could embolden Moscow and other nations with expansionist ambitions.

Meanwhile, Trump escalated his trade war tactics, raising tariffs on steel and aluminium imports to 25% (up from 10%) and eliminating all country—and product-specific exemptions. The measures take effect on 4 March (for now). Yesterday, Trump announced a plan to impose reciprocal tariffs on countries that tax US imports for the sake of 'fairness'. The tariffs would match higher foreign duty rates and counter non-tariff barriers like regulations, subsidies, and exchange policies. The programme, which, like many of Trump's plans, would serve as a negotiation tool, would start with countries with which the US runs a large trade deficit.

Sporadic US policy announcements have once again propelled the gold price to a record high, inching closer to the $3 000/oz mark. Typically, high interest rates dampen gold’s appeal as a non-yielding asset, and the Federal Reserve’s "higher for longer" stance would be expected to restrain the rally. However, persistent market uncertainty – exacerbated by the Trump administration’s shifting tariff policies and unpredictable timelines – continues to drive demand for safe-haven assets. Elsewhere, US stocks declined, while 10-year Treasury yields climbed 10bps to 4.6%. SA’s 10-year bond yield followed suit, rising 11bps. Meanwhile, the JSE Alsi ended the week on a positive note. Gold mining companies have benefitted from this prolonged surge in the gold price.

In currency markets, the rand was largely unchanged against the dollar, though this was more a result of dollar weakness than rand strength. Indeed, the local currency weakened by 0.7% against the euro and 1.3% against the pound sterling. Meanwhile, Brent crude prices slipped as optimism over a potential Russia-Ukraine peace deal raised expectations of a further supply boost in an already well-supplied market.

Next week will be packed with key economic data releases. On Tuesday, Stats SA will publish fourth-quarter unemployment data. Wednesday will be jampacked with January’s CPI, which is expected to have ticked up slightly, along with December retail trade figures released by Stats SA later in the day. January’s CPI will be the first print to fully reflect the changes made to the composition and weighting of the CPI basket, as well as the rebasing. Retail sales have had a strong quarter so far, while momentum is likely to have slowed somewhat in December, the Q4 performance that will be confirmed by next week’s print is likely to be solid.

The most important event will be on Wednesday afternoon when Finance Minister Enoch Godongwana delivers the 2025 Budget Speech. Last week’s State of the Nation Address (SONA) did not signal any major new policy announcements, suggesting the minister will likely maintain his focus on fiscal discipline. Indeed, we do not expect any major surprises in the Budget—clients can click here for our Budget Preview. We will publish a detailed comment for clients on Wednesday.

On the global front, the week begins with Japan’s 2024Q4 GDP data. The economy has now expanded for two consecutive quarters, and this growth, combined with rising inflation, has allowed the Bank of Japan (BoJ) to lift interest rates. In the Eurozone (EZ), on Tuesday, attention will be paid to the ZEW Economic Sentiment Index for February. While there was a slight improvement in January, confidence remains low, particularly in Germany, where a struggling automotive sector and political uncertainty continue to weigh on sentiment. The country’s upcoming federal election later this month will likely end with a coalition government, with the conservative Christian Democratic Union/Christian Social Union (CDU/CSU) currently leading in the polls. However, they may need to form a coalition with Chancellor Olaf Scholz’s Social Democrats (SPD), despite policy differences – the CDU/CSU favouring broad tax cuts, while the SPD advocates higher taxes on high-income earners and a revived wealth tax. Additional EZ data releases next week include flash consumer confidence and February’s flash PMIs.

Meanwhile, both the UK and the US will release their February flash PMIs, with the UK also set to publish January consumer and producer inflation, retail sales, and February consumer confidence.

Roy Havemann

The National Energy Regulator of South Africa (NERSA) approved rules to compensate customers who export excess energy to the grid. This will assist in incentivising the use of renewable energy, particularly rooftop solar. There were some curious components of the rules, including a limitation to the lower of 1 000 kvA or the kvA rating of the supply. Moreover, the rules still provide significant powers to the “distributor” (which is either Eskom or the municipality). They also prescribe that the distributor install the meter, which may appear to lower costs. On the flip side, it may make the process of moving to net billing more onerous.

That said, industry estimates are that up to 6GW of additional electricity capacity is available from households and businesses that could be sold onto the grid. However, this may not support peak demand (which is difficult to meet with solar power). A properly structured tariff (see academic work here and here) would encourage households to draw on the grid to recharge batteries during the day and then be net suppliers over peak periods. This requires further tariff reform work.

This week, the Transnet National Ports Authority (TNPA) further underscored its willingness to partner with the private sector by signing two terminal operator agreements at the Port of Richards Bay.

The first is a 25-year terminal operator agreement with Zululand Energy Terminals (ZET) to develop SA’s first liquified natural gas (LNG) import terminal at the port’s South Dunes precinct. The terminal, which is set to be operational by 2028, will have an initial yearly throughput of at least 2 million tonnes and is being supported by R7bn in investment from the TNPA. This development will help SA deliver on its energy plan to enable 6 000 MW of gas-to-power initiatives by independent power producers and Eskom.

The TNPA also signed a 25-year, R123m terminal operator agreement for a modern liquid bulk terminal to be built and operated at the port by FFS Tank Terminals. It will enhance the port’s capability to handle liquid bulk cargo, particularly bunker fuels essential for maritime logistics.

National Treasury released amendments to Regulation 16 of the Public Finance Management Act (available here). The Regulation governs public-private partnerships (PPPs) and has long been seen as an undue inhibitor of these arrangements. The new regulations take important steps to increase the thresholds (i.e. smaller projects no longer need to meet certain requirements; the exemptions have been improved to ensure good governance; the provision with respect to applications where institutions seek approvals for amendments to PPP agreements has been improved; and a clear framework for receiving and processing unsolicited PPP proposals has been provided together with incentives to ease entry for the private sector).

Unsolicited proposals are those where the private sector comes to the government with a proposal. The previous regulations made this very complex. The reforms should support more private sector investment in much-needed infrastructure.

Nkosiphindile Shange

According to Stats SA, total manufacturing production decreased by 0.4% in 2024 compared to 2023. The most significant contractions came from motor vehicles and transport equipment, which contracted by 13.3% (-1.2%pts) and the metals subsector, which declined by 2.9% (-0.6%pts). On the positive side, the food and beverages subsector saw solid growth (3.7%, +0.9%pts), with chemicals up by 2.6% (+0.5%pts).

In December, production fell by 1.2%, slightly better than the 1.7% contraction expected by the Reuters consensus. On a seasonally adjusted (sa) basis, production fell by 2.4% - this weakness was foreshadowed by a slump in the Absa PMI in December. On a quarterly basis (sa), manufacturing production declined by 0.8% in 2024Q4 compared to 2024Q3, with six of the ten subsectors contracting.

Meanwhile, mining production grew by 0.4% in 2024 compared to 2023. This follows growth of 0.1% in 2023 and a significant decline of 7.8% in 2022. Mining production in December contracted by 2.4% y-o-y, going against expectations for growth in output. PGMs declined by 7.1%, subtracting 2.7%pts, and gold production declined by 8.4% (-1.1%pts). On a m-o-m basis (sa), mining output declined by 3.9% in December. This meant that 2024Q4 production was 0.3% lower than in Q3, with the largest declines coming from manganese (11%, -0.8%pts) and iron ore (4.6%, -0.6%pts). PGMs and coal production both contributed 0.8%pts, as they grew 2.5% and 3.8%, respectively.

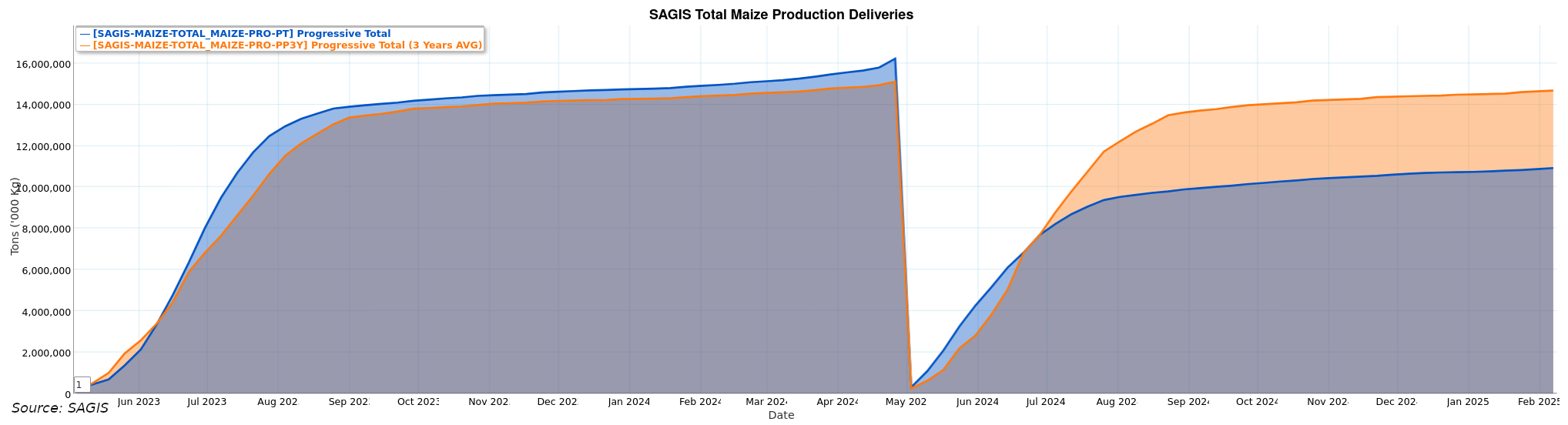

We have recently added selected data from the South African Grain Information Service (SAGIS) to the BER Dataplayground. SAGIS collects data on multiple grains in SA. For now, we have import, export, and production delivery data. In the future, we aim to expand our data collection to include additional datasets, such as monthly reports on stock levels, utilisation and other key indicators, if there is demand.

White maize is a staple food in SA, primarily processed into maize meal (a.k.a mieliepap) for human consumption. Recently, white maize prices have risen sharply due to tight domestic stocks and sustained regional export demand, which was exacerbated by drought conditions in neighbouring countries such as Zambia and Zimbabwe. The chart above illustrates the severity of the production deficit. As of early February 2025, the total accumulated production for the season was approximately four million tonnes below the three-year average.

The annual increase in US headline CPI exceeded expectations of 2.9%, and rose by 0.1%pts to 3.0% in January. Core CPI, which excludes more volatile food and energy prices, also surpassed projections of 3.1%, accelerating from 3.2% to 3.3%. The primary driver behind the rise in headline CPI was the shelter index, which increased by 0.4% m-o-m. Given the substantial weight of shelter costs in the consumer basket, this component alone accounted for 30% of the overall price increase. Additionally, energy and food prices contributed significantly to inflationary pressures, with the gasoline index rising by 1.8% m-o-m and food prices increasing by 0.4% amid a surge in the price of eggs.

Adding to economic concerns, the University of Michigan’s preliminary consumer sentiment index for February fell to 67.8 from 71.1 in January, marking the second consecutive monthly decline. A key factor in this downturn is growing apprehension that the inflationary effects of the Trump administration’s tariff policies may be unavoidable. Inflation expectations for the coming year have surged, reflecting consumers' fears that elevated price levels may persist or worsen.

Several Fed policymakers have emphasised the importance of inflation expectations in shaping monetary policy decisions. If tariff-related concerns continue to drive inflation expectations higher, the Federal Reserve may adopt a more cautious stance on interest rate cuts. Elevated tariffs have the potential to slow economic growth while simultaneously exerting upward pressure on prices.

January’s Producer Price Index (PPI) data further underscored inflationary pressures, registering at 3.5%—the highest rate in nearly two years. This figure matched the revised December rate, which was adjusted upward from 3.3% to 3.5%. The m-o-m PPI increase was 0.4%, surpassing expectations.

These inflation figures follow last Friday’s non-farm payroll report. The U.S. economy added 143 000 jobs in January, which was lower than expected, but the previous months were revised upwards. Indeed, despite the slowdown in job growth, the unemployment rate declined from 4.1% to 4.0%, reaching its lowest level since May 2024.

The UK economy grew by 0.1% q-o-q in 2024Q4, defying market expectations of a contraction. This follows a stagnant Q3 performance. The unexpected expansion was primarily driven by increases in the services and construction sectors, which grew by 0.2% and 0.5%, respectively. In contrast, production output declined by 0.8%. Concurrently, retail sales increased by 2.5% y-o-y, down from 3.1% in December but above market expectations of 0.2%.

Editor: Lisette IJssel de Schepper

Tel: +27 (0)21 808 9755

Email: lisette@sun.ac.za

Click here for previous editions of this publication.

Please refer to the glossary on the BER website for explanations of technical te

Friday, 14 Feb 2025