General

Publications & Data

Join the conversation

Social Links

Social Links

Lisette IJssel de Schepper

Most of the domestic data releases were a bit disappointing. The week started with another below-50 Absa PMI print, with the S&P Global PMI on Wednesday also stuck in negative terrain in February. From a GDP growth perspective, while the economy rebounded from the 0.1% quarterly contraction in Q3, the 0.6% recorded in Q4 is hardly something to celebrate. Indeed, while the consumer was strong, as expected, and there was an uptick in private sector fixed investment after three quarters of decline, the overall print was uninspiring. The fact that the annual economic growth rate slowed to 0.6% from 0.7% in 2023 is bleak. Unfortunately, the RMB/BER Business Confidence Index (BCI) for Q1 does not point to a strong further recovery in Q1, with sentiment unchanged at 45 index points. To be fair, activity ticked along, so the economy may, too, in Q1, but it certainly does not point to a meaningful acceleration. On the bright side, local vehicle sales did well in February, but exports slumped. This does not bode well for the Q1 current account, which stayed in deficit in Q4 – although coming in smaller than expected.

On the global front, following initial delays, US tariffs of 25% on most Canadian and Mexican imports came into effect on Tuesday, and an additional 10% was imposed on China. This impacts about $1.5 trillion in annual imports. The day before, the US S&P500 saw the worst sell-off of the year when US President Donald Trump confirmed that the 25% tariffs against America’s biggest trading partners would definitely happen. Indeed, since the start of his presidency, bonds have now performed better than equities, with the S&P500 having wiped out all of the gains since the elections. Canada was quick to implement targeted countermeasures. China retaliated by, among other measures, imposing levies of up to 15% on some US agricultural products. Trump says that more tariffs are to come, including the reciprocal tariffs expected in April, defending the use of tariffs in general during his address at a joint session of Congress. However, US Commerce Secretary Howard Lutnick said that the US could walk back some tariffs on Mexico and Canada. Indeed, American car manufacturers were later exempt from the 25% tariff for a month. Additionally, Lutnick yesterday suggested that all goods that met the rules of the 2020 free trade deal would be granted a one-month reprieve. Trump later confirmed this arrangement for Mexico and Canada. Still, despite two U-turns in policymaking, concerns that the tariffs may hurt US growth mean that traders have now added to expectations of US rate cuts in 2025, with three 25bps cuts now fully priced in and the first cut possible in May. This is despite a likely tariff-induced uptick in inflation.

Last Friday, during an awkward exchange (from an outsider’s perspective at least) between President Trump, his Vice President JD Vance, and the Ukrainian President Volodymyr Zelensky, the countries ended up not signing the minerals deal. Trump ordered a pause in all military aid to Ukraine. The aid will remain suspended until Trump decides that a good-faith commitment to peace has been made. The US also said America would stop intelligence-sharing with Ukraine. Ukraine reportedly sent a letter to the US that it would be willing to sign the minerals deal and talk about peace.

European stock markets hit record highs early this week as leaders committed to ramping up defence spending and supporting Ukraine. Defence stocks surged, with the German DAX rising by 3.4% on Monday—the biggest one-day increase since 2022. Later in the week, European stocks moved lower amid concerns that the continent could be Trump’s next target, with European automakers, especially under pressure. However, reports that the German chancellor-in-waiting seemed to have the support to essentially change the constitution to allow for increased borrowing for infrastructure and defence spending were seen as a positive for the region (and the euro, which strengthened significantly against the dollar). German bond yields spiked, which filtered through global bond markets and pushed the Japanese 40-year bond yield to the highest level since its inception in 2007. Even in the US, where worries about the impact of tariffs on the economy initially pushed bond yields lower, they rose later in the week. Meanwhile, the European Central Bank (ECB) cut its policy rate for a sixth time since June last year, but it is less certain how it will proceed from here with the US pulling back from Ukraine and European countries seemingly ready to spend more on defence.

In China, the government announced it would again target ‘about 5%’ growth in 2025. It did, however, lower its inflation target from 3 to 2%, which is the lowest target in 20 years. Still, given that consumer inflation averaged 0.2% over the past two years, it will not be easy to reach 2%. The 5% growth target will also not be an easy feat and will likely require significant stimulus, especially with the possibility of a trade war weighing on growth. Indeed, the country raised the headline budget deficit target from 3% to 4% of GDP – the highest level in about three decades - and said it would increase its defence budget.

In commodity markets, OPEC+ said it would increase oil output by 138 000 barrels per day in April. The announcement was unexpected and pushed oil prices sharply lower. Over time, the cartel plans to ramp up production by 2.2 million barrels per day by 2026 – but it stresses production increases can be paused or reversed subject to market conditions. Meanwhile, the gold price hovered just below a record high ($2 958). Silver is also benefitting from safe-haven demand.

The National Budget is scheduled to be tabled on Wednesday. A statement from Monday’s special cabinet meeting seems to suggest that the cabinet has provided its final input into the Budget and that the Finance Minister and National Treasury are set to finalise it. According to Business Day, a 0.75%pt VAT hike is one of the options considered. Another option would be to withhold the employer portion of payment to the Government Employees Pension Fund (GEPF) for a year, which could raise about R53bn once-off. As usual, we will publish a comment on the Budget details for clients.

On the data front, mining and manufacturing production figures for January are due on Thursday. Mining slumped by more than expected in December, while manufacturing also came out weak. Worryingly, the Absa PMI remained subdued in January, which suggests that a sharp rebound in manufacturing output is unlikely at the start of the year. This week’s electricity production data showed a monthly uptick of 0.4% in January and was still significantly up (5.7%) compared to the load-shedding-ridden-January of 2024 – this base effect boost should fade after March. The Stats SA electricity production data now also includes electricity wheeling from IPPs, small now, but hopefully a bigger contributor over time.

Later today, US jobs data will be in focus. The surveys took place a week before Trump’s administration fired federal workers across agencies, so this should not (yet) be reflected in February’s data, while other labour market estimates are mixed. Bloomberg polling shows guesses within a wide range of 30 000 to 300 000 job gains. Wednesday’s consumer inflation figure for last month will be the most watched US data release next week. The monthly rate of increase is set to slow slightly from January’s 0.4%, but this still leaves annual inflation unchanged at 3.3%. Factory-gate prices are set to follow on Thursday, with the m-o-m rate expected to remain unchanged at 0.4%.

On the monetary policy front, the Bank of Canada (BoC) meets on Wednesday. The BoC cut its policy rate by 25bps in January and is expected to continue easing in 2025 to mitigate the negative impact of US tariffs on the economy. A full outlook update is scheduled for its April meeting.

Katrien Smuts

According to Stats SA, the real GDP growth accelerated to 0.6% q-o-q in 2024Q4, below consensus expectations. This weaker-than-expected print pulled full-year growth down to 0.6%, slightly lower than the 0.7% recorded in 2023. There were notable revisions to 2024Q3 GDP. Stats SA now estimates that the economy contracted by just 0.1% q-o-q (previously -0.3%), mainly because the agriculture industry's contraction was revised to -19.7% from -28.8%. Clients can click here for our detailed comment.

As expected, lower inflation, interest rate cuts, and the two-pot retirement withdrawals supported consumer-linked industries. However, these gains were not enough to offset contractions in other sectors. Indeed, as in Q2 and Q3, household consumption was the main driver of growth from the expenditure side, adding 0.6%pts on the back of a 1% q-o-q expansion. Exports also contributed positively (+0.5%pts), but all other expenditure components contracted. Fixed investment was a notable disappointment, declining again after a brief uptick in Q3, but at least the private sector component ticked up.

The SA Reserve Bank’s latest balance of payments data indicates that the current account deficit narrowed in 2024Q4. As a percentage of GDP, the deficit narrowed from (a revised) 0.8% in Q3 to 0.4% in Q4. The primary driver behind the smaller current account shortfall in Q4 was an improved trade surplus, which grew from R200.4 billion in Q3 to R232.9 billion in Q4. For the year as a whole, the current account deficit narrowed from 1.6% of GDP in 2023 to 0.6% of GDP in 2024.

After three consecutive increases, the RMB/BER BCI remained unchanged at 45 index points in 2025Q1. While slightly above the long-term average of 43 and well above early 2024 levels, it is concerning that confidence declined in four of the five sectors. The exception was new vehicle dealers, where confidence surged by 29 points, fully offsetting declines in all other sectors. This came despite the composite activity indicator remaining at an elevated level and even ticking up slightly from Q4. Encouragingly, many respondents are fairly optimistic about the next quarter. However, for confidence to rise meaningfully, we need to see a sustained recovery in demand and activity or firm progress on the structural reform front.

The Absa PMI edged down by 0.6 points to 44.7 in February, while the S&P Global PMI ticked up from 47.7 to 49.0. Despite the latter’s improvement, both indices remain below the neutral 50 mark, signalling continued contraction in the manufacturing sector. Key underlying components worsened, with new orders and employment declining in both surveys. Business activity, often linked to new business inflows, also slowed in February. Notably, both PMIs recorded a slight uptick in the purchasing price indices, reflecting higher input costs due to rising fuel prices and a weaker rand, particularly early in the month. Additionally, survey respondents highlighted concerns over escalating SA-US tensions, which are weighing on business sentiment.

Naamsa’s latest report indicates that domestic new vehicle sales increased by 7.3% y-o-y in February 2025. The overall performance was driven by a strong rebound in passenger vehicle sales, which rose 16.8% y-o-y to 33 757 units. The acceleration in sales reflects several supporting factors, including easing (domestic) inflation, some interest rate cuts, improved consumer sentiment, and a boost in disposable income following the implementation of the two-pot pension withdrawal system in September last year. By contrast, vehicle export sales remained under pressure, contracting 8.6% y-o-y to 34 656 units in February. The decline comes amid heightened global trade uncertainty and weaker demand from key trading partners.

Hanjo Odendaal

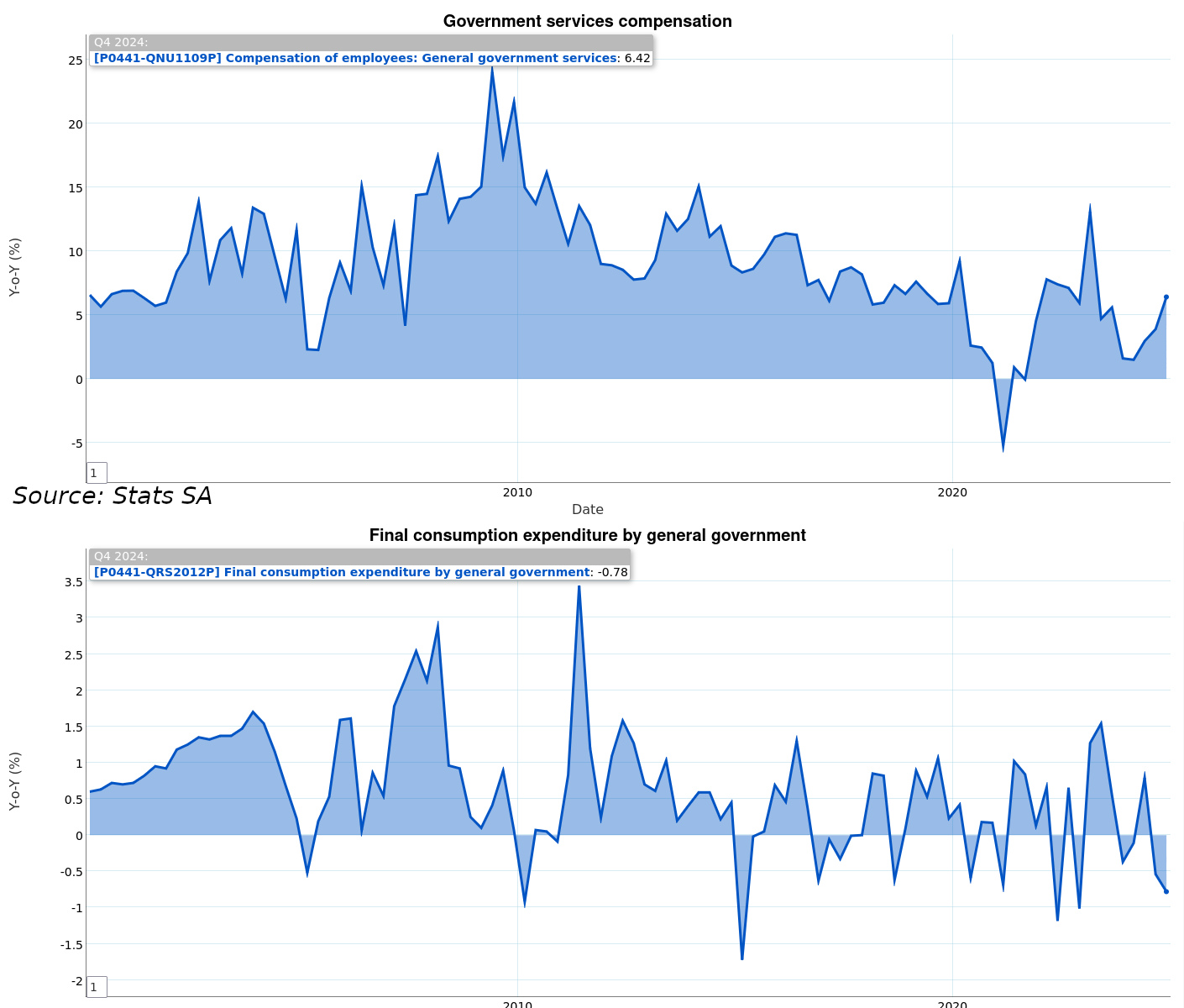

Real final consumption expenditure by the general government declined by 0.8% y-o-y. However, (in nominal terms) compensation for employees in general government services increased by 6.4% over the same period. This rise reflects upward adjustments in wages and employment-related benefits, despite an overall decline in employment within national and provincial government sectors. While the government is tightening its belt, rising personnel costs add to expenditure.

Data sourced from the BERDataPlayground

Data sourced from the BERDataPlayground

Nkosiphindile Shange

The ECB announced a widely anticipated 25bps rate cut in March. However, there was a change in tone, signalling a more hawkish stance moving forward, meaning that there is a possible slowdown or pause in interest rate cuts moving forward. Consumer inflation has fallen from a peak of 10.6% in October 2022 to 2.4% in February. However, the ECB revised its inflation forecast upwards due to higher energy costs and expects inflation to average 2.3% in 2025, 2026 (1.9%), and 2027 (2%). Domestic inflation remains higher than the 2% medium-term target due to higher wages and prices adjusting to past prices and delaying to reflect current conditions. Another upward risk to Eurozone inflation is the possible hundreds of billions of euros that Germany’s Chancellor-in-waiting plans to unleash to boost defence and infrastructure spending.

The JP Morgan Global Composite PMI edged down to 51.5 index points in February, from 51.8 in January. The current reading is a 14-month low; however, this output reading remained above the 50-point mark for 25 consecutive months, signalling a sustained expansion. The global services sector continues to outperform the manufacturing sector; however, the slowdown in the services sector has made the current levels have the least outperformance since services overtook manufacturing in January 2023. Manufacturing production rose at the quickest pace since June 2024.

In the US, the ISM Manufacturing PMI fell to 50.3 points in February from 50.9 in January. There was slower growth as the demand eased and production stabilised. Manufacturers were cutting down staff, and the tariff changes sent operational shocks across the sector. Positively, the US ISM Services PMI increased unexpectedly to 53.5 points in February from 52.8 in January.

The HCOB Eurozone Composite PMI Output Index came in at 50.2 points in February, unchanged from January. Demand conditions within the EZ remain poor, and the volume of new business shrank further. The HCOB Eurozone Services PMI Business Activity Index declined to a three-month low of 50.6 in February from 51.3 points in January.

The Caixin China General Manufacturing PMI improved to a three-month high of 50.8 points in February due to higher output and new orders as market conditions improved. This is the fifth consecutive month that the PMI has edged above the 50-point mark. The Caixin China General Services PMI showed that the services sector continued to expand in February, as the index edged 51.4 compared to 51 points in January. This is the 26th consecutive month that the services PMI edged above the 50-point mark.

Editor: Lisette IJssel de Schepper

Tel: +27 (0)21 808 9755

Email: lisette@sun.ac.za

Click here for previous editions of this publication.

Please refer to the glossary on the BER website for explanations of technical terms

Friday, 07 Mar 2025