General

Publications & Data

Join the conversation

Social Links

Social Links

Lisette IJssel de Schepper

After originally being scheduled for 19 February and then postponed at the last moment, the National Budget for 2025 was tabled by the National Treasury (NT) on 12 March. This is not to say it will be a done deal from here, the DA has already indicated that it will not support the Budget in its current form. In some ways, Budget 2.0 was largely the same as Budget (1.0). While the contentious 2%pt-VAT hike was watered down to 0.5%pts increases spread over two years (so 1%pt in total), it still comes with a heavy tax burden, largely shouldered by the consumer. The net impact of the proposed tax adjustments - which, in addition to the VAT hike, include not adjusting income tax brackets or medical tax credits for the second year in a row - will take R28bn out of the hands of consumers in the coming year, and almost R120bn over three years. There was little change in expenditure plans relative to Budget 1.0.

The Budget(s) presented in 2025 represent a shift in the fiscal stance. From spending cuts announced in 2024, fiscal consolidation would now happen through higher taxes paying for more expenditure (instead of borrowing). Indeed, in Budget 2.0, consolidated non-interest spending will now grow by 0.8% on average annually in real terms over the medium term (compared to 0.9% in Budget 1.0), from the contraction planned for in Budget 2024. Despite this shift, the National Treasury said in the Budget Review that “the fiscal strategy remains on track,” although it admitted that “fiscal buffers are weaker, including due to a smaller contingency reserve.” Weaker buffers at a time of rising global uncertainty are obviously a cause for concern. It is also troubling that the Budget was not really positive for economic growth – which is what we actually need to get out of the fiscal stranglehold.

Clients can find our summary of the Budget and initial verdict (which is not so positive), here.

This week’s domestic data batch suggests that the economy had a mixed start to 2025 – but certainly not the bump required to see a significant growth boost. Indeed, we have downwardly revised our growth outlook for 2025.

For more on our latest macro view (incl. the interest rate), clients can click here for a comment.

Business Day readers can read a shortened version of our view in today’s BER column, here.

On the global front, US tariff threats (including a 200% tariff on French champagne), announcements and implementations resulted in the first serious retaliation from trading partners. Mark Carney, who will be sworn in as prime minister of Canada later today, said he would meet with Trump as long as Canada’s sovereignty is protected. In other political news, votes in Greenland unexpectedly backed a party that wants a slower route to independence (following the US’s threat to take over the country). Back to trade, it is impossible to keep track of all the announcements and reactions in an SA-focused Weekly, but it is safe to say that the trade war is heating up. The Russia-Ukraine war, however, may be edging closer to a ceasefire deal. Ukraine is reportedly ready to accept a 30-day ceasefire, while talks with Russia have started – although some argue that Russian President Vladimir Putin is likely to drag these out.

The selloff in US equities continued, with tech stocks with high valuations, big banks, and airlines—the latter two exposed to a consumer slowdown—suffering the most. Yesterday, the S&P 500 again sank into so-called correction territory (as it did briefly on Tuesday too), which means it is more than 10% down from a record high just three weeks ago. Last week, the Nasdaq confirmed it is in a correction by closing 10.4% lower than its all-time end of day high achieved mid-December. The JSE Alsi dipped by just over 1% last week, while the rand moved weaker against all major currencies.

The Brent crude oil price rose by 1.7% w-o-w, but stayed close to $70/barrel and is about $10/barrel lower than this time in January. For now it seems unlikely that prices will spike much higher. As per the International Energy Agency, the escalating trade war is threatening demand just as OPEC+ is planning to reverse earlier output cuts.

Due to Friday being a public holiday, a somewhat shorter version of the Weekly Review will be published after the SA Reserve Bank’s (SARB) interest rate decision late Thursday afternoon. Clients will receive a more detailed comment on the SARB’s decision, also on Thursday.

Even though next week will be shorter due to the public holiday, it will still be a big one for the domestic data calendar. The BER Inflation Expectations Survey for Q1 will be released on Monday. This, coupled with next week’s consumer inflation print for February, will be important input for the SARB interest rate decision on Thursday. On consumer inflation, we see annual inflation ticking up from 3.2% to about 3.7% in February on the back of a fairly steep m-o-m increase. A big reason for the steep monthly uptick is that medical aids were surveyed in February, and this should increase by about 11% y-o-y – in line with announced premium increases – which bumps up the monthly increase above 1%. Stats SA will publish internal trade data for January. The consumer had a strong close to 2024, so it will be interesting to see how that momentum carried through into 2025.

Following the hawkish tilt in January, we think the SARB is likely to keep its interest rate unchanged next week as the SARB likely remains highly concerned about the potential upside risks to inflation. Furthermore, only time will tell by how much, but the VAT hike(s) will be inflationary. Should actual inflation continue to undershoot, inflation expectations remain well behaved, and the US Fed resumes its cutting cycle, the SARB may be tempted to cut again later this year. For more on our latest macro view (incl. the interest rate), clients can click here for a comment.

The US Fed announces its interest rate decision the day before the SARB, but is unlikely to make any changes this time. However, the probability of a rate cut in May is now essentially a coinflip and markets have repriced in about three 25bps rate cuts this year. This week’s lower-than-expected consumer inflation print (see international for more) is helping the odds of a cut later this year. Staying in the US, markets will watch Washington to see whether a government shutdown can be averted. The stopgap funding bill that extends most current spending levels until 30 September still needs to be passed by the Senate, where Trump’s Republicans will need a handful of Democrats to vote in favour of it for it to pass. Senate Democratic leader Chuck Schumer says this will not happen, and is trying to convince the Republicans to agree to a Democratic plan to provide funding through April 11 instead. Early Friday morning (SA time), reports suggested that the two parties were starting to agree to avert the shutdown. This was positive for market sentiment, with Asian stocks and US futures picking up this morning.

Mining production fell by 2.7% y-o-y in January, following consecutive declines of 0.9% in November and 2.4% in December. On a seasonally adjusted (sa) basis, production contracted by 1.2% in January, following a 3.7% drop in December. The annual decline was primarily driven by sharp decreases in the production of iron ore (-15.1%, contributing -2.7%pts), PGMs (-2.8%, -1.1%pts), and coal (-4.4%, -1%pts). In contrast, manganese ore was the largest positive contributor, rising by 21.2% (1.2%pts).

Like mining, manufacturing production declined on an annual basis. Output fell by 3.3% y-o-y in January after decreases of 1.9% in November and 1.2% in December. However, on a monthly basis, output increased slightly by 0.2% (sa). The biggest drag was the petrochemical subsector (-9.1% y-o-y, -2.1%pts), food and beverages (-3.2%, -0.8%pts), and transport (-10.1%, -0.8%pts). The largest positive contributor was wood and paper, which grew by 5.6%, adding 0.6%pts.

So, to summarise, electricity (released last week) and manufacturing production edged up slightly on a monthly basis in January, but mining output declined. It also remains to be seen how the closure of ArcelorMittal’s longs business will work through the industrial side of the economy and what the (negative) knock-on thereof will be.

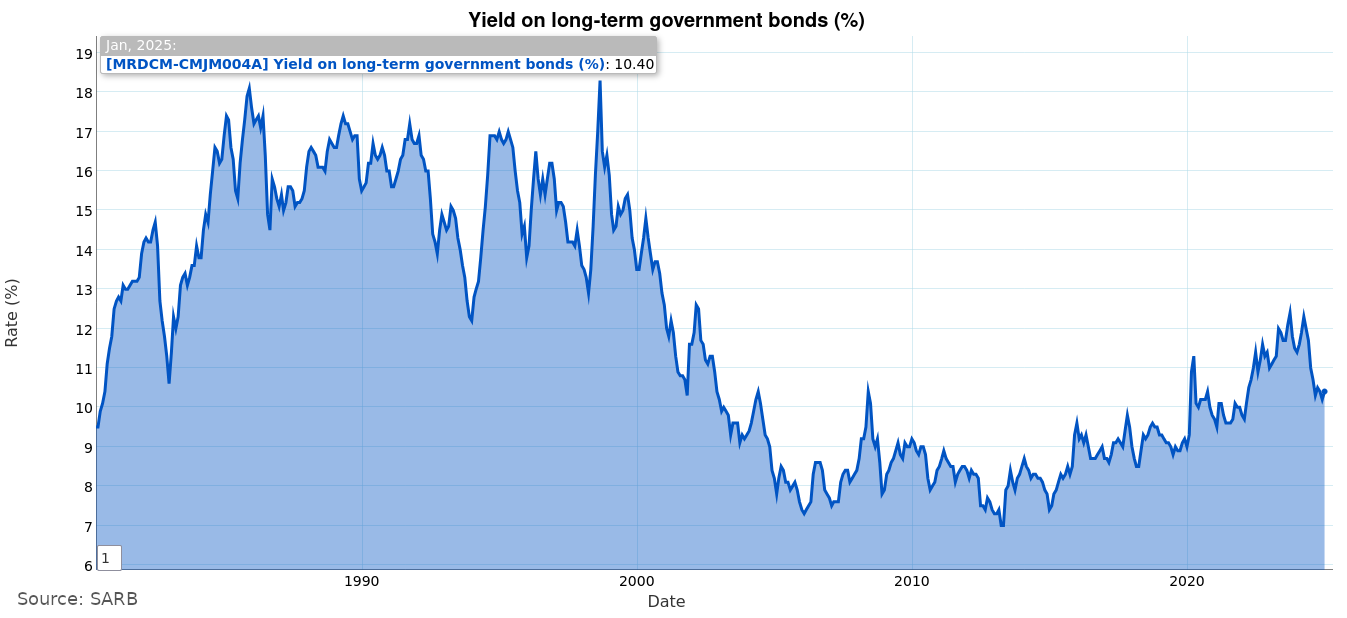

Long-term government bond yields reflect investor sentiment, responses to shifts in inflation expectations, monetary policy and global volatility. Rising yields typically signal concerns over inflation or fiscal risks (with bond prices moving inversely from yields and thus falling), while declining yields may indicate improved confidence or increased demand for safe assets amid uncertainty.

SA's 10-year government bond yields rose in early 2024, peaking at 12.3% in April, before steadily declining in the second half of the year. By December, yields had fallen to 10.2% - suggesting stronger demand for government bonds. Lower inflation expectations and improved investor sentiment potentially drove this. A modest uptick to 10.4% in January 2025 hints at stabilisation, although future movements will depend on global political instability, broader economic conditions and monetary policy decisions.

Data sourced from the BERDataPlayground

Data sourced from the BERDataPlayground

The US CPI inflation rate slowed to 2.8% y-o-y in February, down from 3% in January, according to the latest data from the US Bureau of Labor Statistics. Food prices rose by 2.6% y-o-y, with the egg price index surging by 58.8%. The spike is linked to a severe avian flu outbreak, which has led to large-scale culling of egg-laying hens, restricting supply. This echoes the egg price shock SA experienced two years ago under similar conditions. Some US grocery stores have even introduced purchase limits to curb demand and prevent further price hikes. However, supply-demand dynamics should normalise by mid-year.

Meanwhile, energy prices declined by 0.2% y-o-y, mainly due to lower gasoline prices. Core inflation also eased, dipping to 3.1% from 3.3% in January. Encouragingly, shelter inflation (owners’ equivalent rent and actual rent) rose by just 4.1%, its slowest pace since December 2021. Given shelter’s significant role in persistent core inflation, this moderation is a positive development for the inflation outlook. However, disinflation in shelter alone will not be enough to bring headline CPI back to target levels. With renewed inflation risks on the horizon, the Fed will remain cautious as it deliberates its policy decision next week. It is expected to hold policy rates steady at next week’s FOMC meeting.

Job openings edged up slightly to 7.7 million in January, with the jobs-per-unemployed worker ratio ticking modestly higher to 1.13. This is a relatively positive result, given the policy and economic shifts that have since unfolded.

However, labour market uncertainty has risen sharply in recent weeks. The Challenger Report recorded nearly 180 000 job cut announcements in February—the highest since July 2020 and the worst February print since 2009. Government job cuts dominated, with 62 000 layoffs, though private sector cuts also picked up. The non-farm payrolls report also showed weakness recently, with Federal government employment falling by 7 000 in February, following a hiring freeze for certain positions. This contrasts with the previous six-month average increase of 3 000 per month.

While January’s job openings data suggested some stability, gross hiring rates have slowed, leaving little room for meaningful net employment growth. Given the latest trends, labour market conditions are unlikely to strengthen materially in the near term.

Eurozone’s industrial production rose by 0.8% m-o-m in January. Industrial production has been very morose over the last 18 months, so a slight pick-up is encouraging, even though it is too early to tell whether this signals a strong turnaround in this sector. That said, policy support could provide some momentum. Last week, Germany unveiled a major fiscal package aimed at boosting defence and infrastructure spending. If implemented effectively, this could support industrial activity and economic growth across the bloc in the coming years. On an annual basis, industrial production remained flat, highlighting the ongoing challenges in the sector.

Editor: Lisette IJssel de Schepper

Tel: +27 (0)21 808 975

Email: lisette@sun.ac.za

Click here for previous editions of this publication.

Please refer to the glossary on the BER website for explanations of technical terms.

Friday, 14 Mar 2025